Australia’s embrace of remote work—now pervasive with 40% of workers in hybrid or fully remote working arrangements, reports the Australian Bureau of Statistics—is quietly pushing small and medium-sized enterprises (SMEs) to the brink.

The latest CreditorWatch Business Risk Index for February 2025 reveals a grim reality: while rising costs hammer profitability, it’s the deserted Central Business Districts (CBDs), abandoned by telecommuting employees, that are delivering a devastating blow. Hospitality closures have soared to a record 9.3% nationwide—one in 11 businesses shuttered in the past year—up from 7.1% in 2024, with insolvencies climbing across the country. This transformation, once hailed as a agile future, is proving to be a quiet killer for urban foot-traffic-reliant SMEs, and one that poses desperate questions about their sustainability in an economy that has become remote-first.

ACT’s ‘recession-proof’ reputation unfolds

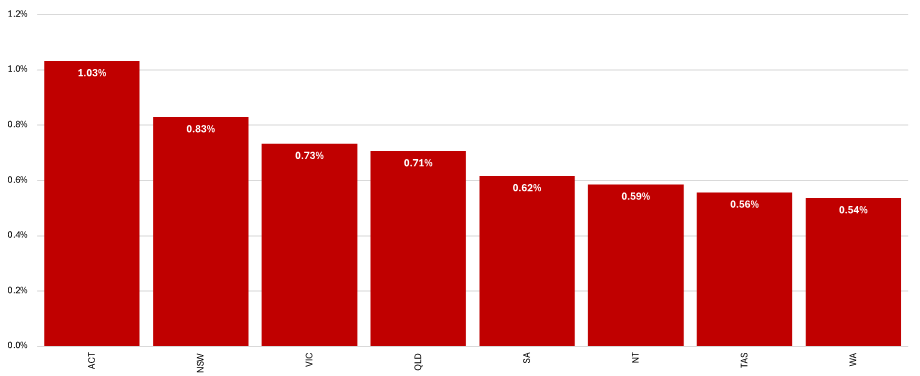

The Australian Capital Territory (ACT), long regarded as recession-proof because of its stable public sector jobs, has proven to be an unexpected casualty. CreditorWatch statistics show the ACT surpassed Victoria in February 2025 insolvency levels, a shock given Victoria’s weaker economic performance, the National Australia Bank (NAB) Business Confidence Survey (March 2025) reported. Why? Government employees, the bulk of the ACT’s workforce, have reduced CBD foot traffic with their shift to remote work. The ABS notes that public administration and safety workers, a key ACT cohort, have shifted heavily to remote setups, with 45% working from home at least part-time in 2024—up from 20% pre-pandemic.

This exodus has hit SMEs hard. Hospitality closures in the ACT reached 9.3% in the 12 months to February 2025, with food and beverage businesses bearing the brunt. ABS Consumer Price Index data show food prices rose 3.5% year-on-year, and the Reserve Bank of Australia (RBA) reports discretionary consumer spending declined 4% since 2023 due to cost-of-living pressures. In Canberra’s Civic precinct, cafes and lunch spots that once depended on office workers now have empty tables. The CreditorWatch report says this is not just confined to the ACT—this is also being experienced in Sydney and Melbourne CBDs—but the overreliance of the ACT on one workforce makes the hit worse.

ABS Counts of Australian Businesses identifies that the ACT is home to 29,000 SMEs, 60% of which operate in service industries like hospitality and retail—sectors most affected by reduced physical visitation. With CBD resurgence impossible in the event of hybrid work, ACT SMEs will likely look towards residential suburbs where they can service remote workers through delivery services or pop-ups, or go online to tap a broader market.

Rising defaults signal deeper economic strain

The ripple effect of remote work extends well beyond the ACT, stretching SMEs nationwide. CreditorWatch reports a 47% year-on-year increase in business-to-business (B2B) invoice payment defaults—a dire indicator of cash flow pressure. Companies that default on payments see their insolvency risk rise by 0.7% to 7.9% over a 12-month period, a trend reinforced by the RBA’s Small Business Economic and Financial Conditions Bulletin, which notes SMEs to have smaller financial buffers than large companies. NSW also recorded greater insolvency levels than Victoria in February, maybe as a result of economic spill-over from the fall in Victoria, while Western Australia’s economy based on mining continued its rates lowest, with a 2.1% unemployment rate (ABS, February 2025).

The move to remote working contributes to other pressures. Electricity prices have risen 10-15% each year, and rents near CBDs are increasing as landlords fill gaps—slapping SMEs that are not able to shift easily. The ATO Taxation Revenue report confirms that SMEs’ tax debts have increased by 15% since 2022, as the majority of companies are still repaying pandemic-related deferrals. While office staff stay at home, city SMEs are facing a two-way squeeze: less customers and higher bills. The RBA indicates that the hospitality and retail sectors that employ 2.5 million Australians (ABS, 2024) are particularly at risk, with insolvency rates in these sectors now above pre-pandemic levels.

SMEs can resist this with credit risk tools—CreditorWatch’s system, for instance, tracks client payment records—or by negotiating more stringent payment terms. The ATO provides payment plans for tax debt, a last resort for struggling companies, though take-up remains at 25% of qualifying businesses (ATO, 2024).

Embracing the new reality

Working from home is re-mapping Australia’s economic landscape, and SMEs must adapt or perish. High-risk locations like Western Sydney and South-East Queensland have an estimated 7.9% failure rate in areas like Bringelly-Green Valley, CreditorWatch reports, based on construction problems and lower incomes. Of the CBDs, Adelaide is lowest risk at 5.1%, followed by Perth (5.2%), Melbourne and Brisbane (5.8%), and Sydney (6.2%). Adelaide’s SME base—less office-based trade-oriented—is supported by regional stability, while Perth rides WA’s mining boom. Recent relief measures bring a glimmer of optimism.

The RBA’s rate cut in February 2025—the first since 2020—reduced borrowing costs, and mid-2024 tax cuts contributed 2-3% to family incomes. Storm clouds gather, though: mooted US tariffs would trim 1% from world growth as per the International Monetary Fund, 2025, testing Australia’s export-driven economy and potentially nudging unemployment up from 4.1% to 4.5% by the end of the year. With ATO tax liabilities a growing burden, SMEs face a grim choice: evolve or become one of the 436,018 that departed in 2023-24.

Action is what survival relies on. Diversifying revenue streams—e-commerce or suburban pop-ups, for example—can offset CBD losses. Building cash buffers, as the RBA suggests in its Financial Stability Review (March 2024), shields from shocks, with 25% more cash than pre-pandemic SMEs being instructed to retain that edge. The ATO’s SME Recovery Loan Scheme (2023) offers low-interest loans, but only 10% of eligible companies have availed themselves of the offer (ATO, 2024)—an opportunity lost to bridge the gap.

Australia’s SMEs, with 2.6 million and employing two-thirds of the country’s workforce are the lifeblood of the economy. Remote work’s quiet destruction—empty streets, unpaid invoices, and shuttered shopfronts—demands a solid reconsideration.

Data Sources: CreditorWatch Business Risk Index, ABS Labour Force Survey, ABS Counts of Australian Businesses, RBA Bulletins, ATO Taxation Revenue, NAB Business Confidence Survey

Keep up to date with our stories on LinkedIn, Twitter, Facebook and Instagram.