Businesses around the world must wait further developments on the US tariff policy front, likely keying off the announcements of the results of the first trade negotiations between the US and India and the US and Japan in coming weeks.

The Federal election and Australian businesses are effective bystanders in this process, though helpfully CreditorWatch expects the RBA to reduce the cash rate a further 25bps on May 20 as the Q1 CPI confirmed underlying inflation continues to moderate.

It will remain an uncertain time for business over the next few months, and one where credit checks will be even more important given the many interconnections in the global economy that may be impacted by these tariff changes, be they temporary or more permanent. Insolvencies are likely to remain generally elevated due to previous cost pressures and could reach new highs if tariff policies are not reversed or lessened.

Overall economic growth and business activity is likely to be slower – substantially if the current very high level of proposed tariffs on many countries is permanently implemented – though that still seems unlikely.

The Past Month

April was dominated by the financial market volatility and weakness and the subsequent events that followed the 2 April announcement of reciprocal tariffs by President Trump. These included substantial escalation in the bilateral tariffs between China and the US and some high-profile backtracking and temporary exemptions by the US.

Share markets initially plunged as markets priced increased risks of US recession, though much of these moves reversed as the month progressed and various partial backtracks occurred.

Economic data for the most part – unsurprisingly – took a back seat, reflecting business conditions that applied prior to April’s policy changes. US consumer and business confidence measures have begun to reflect increased uncertainty. These surveys and indications of labour hiring/firing intentions are likely to be key in the weeks ahead. However, it’s likely the economy will still be well ahead of the data – already there are reports of 30-50% of shipping bookings being cancelled between the US and China, and of 20-30% y/y reductions in Canadian visitation to the US.

The situation is chaotic, with the ultimate level of tariffs and the longevity of the current level very uncertain. Current bilateral levels between the US and China are clearly unsustainable. US businesses would be hard pressed to forecast the outlook six weeks ahead let alone six months in advance, which will likely see businesses delay hiring and investment decisions, contributing to a slowing in US economic activity, which is never a positive development for Australia or the world.

Not surprisingly, there was very little focus on Australian economic data this month, and even the election campaign was watered down for much of April from a media coverage perspective. Australia received the equal lowest 10% reciprocal tariff rate, which puts us at a relative advantage to other countries with higher tariffs, especially as the US is a small export market for us.

The larger impact for Australia was always going to be indirect, reflecting the impact of higher tariffs on US, Chinese and global growth, on consumer and business confidence and via wealth effects via reduced share prices. These effects will take some time to become clear. Yale University’s Budget Lab estimated that US economic growth could be reduced by 0.9 percentage points in 2025 by the April 2 reciprocal tariffs, placing the US economy dangerously close to recession, unless tariff and trade restrictions are relatively quickly lessened.

For the record, Australian developments of note during April were:

- The unemployment rate remained very low at 4.1%.

- The Reserve Bank Board signalled it would review monetary policy settings at its May Board Meeting, where it would have more information on tariff developments, a full set of new forecasts, and importantly the March quarter CPI outcome.

- The March quarter CPI showed a 0.7% q/q increase in the important trimmed mean measure of core inflation. This brought the annual rate of core inflation to 2.9%, the first time core inflation has been in the RBA’s 2-3% target band since late 2021.

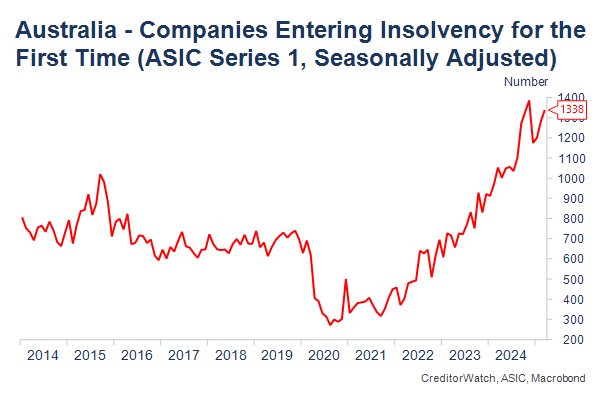

- Final insolvency data for March – in keeping with CreditorWatch proprietary data on B2B Trade Payment Defaults – revealed insolvencies remaining at relatively elevated levels, but not exceeding the highs recorded in late 2024. Prior increases in costs for both consumers and businesses and accumulated tax debts are the key forces pressuring businesses, though income tax cuts and the first RBA interest rate reduction have likely provided some assistance in recent months.

The Month Ahead

Normally, with a federal election imminent, a month ahead comment would be packed full of comment about the contrasting policies of the Labor and Coalition parties. The election has been overtaken by global events, which should be the dominant focus of businesses and policy makers, including the RBA. There do not appear to be huge policy differences between the two major parties, with the Opposition’s nuclear energy plans perhaps the starkest difference. Both parties recognise the importance the increased cost of living is having on voters, with different approaches to providing assistance: Labor through permanent small tax cuts and the Coalition largely through temporary fuel tax relief and an income tax offset. While either will provide useful support to consumers and in turn for businesses, both are likely to be small in relation to the potential economic and business impacts that will flow from the impact of US tariff policies.

CreditorWatch expects the Reserve Bank Board to lower the official cash rate another 25bps on May 20, given the continuing progress being made in reducing the rate of inflation. Note the latter does not mean that prices are falling or that the cost of living or of doing business has reduced. These pressures will mean insolvencies remain relatively elevated and suggests interest rates were going to fall in any case by another 50bps this year. Additional flow-on negative effects on global economic activity from US tariff policy – if not quickly reversed or lessened – would likely see insolvencies rise to new highs, and larger interest rate reductions occur over the next year.

This leaves Australian businesses in much the same situation as businesses in the rest of the world – watching the chaotic policy announcement and subsequent back pedalling and deal making dynamic of the Trump Administration on tariffs. Complex interlinkages in the global trading system – and slower economic activity in the months ahead – reinforce the importance of having strong credit processes in place to deal with these uncertain business conditions. Some opportunities may of course arise for Australian suppliers to Chinese customers as a result of current very high Chinese tariffs on US imports – and for Australian businesses to source some products offshore at cheaper prices from producers in tariffed countries.

By Ivan Colhoun, Chief Economist, CreditorWatch

Keep up to date with our stories on LinkedIn, Twitter, Facebook and Instagram.