The ATO has published detailed guidance on how Payday Super works in practice, including what happens to overpayments, rejected contributions and late payments.

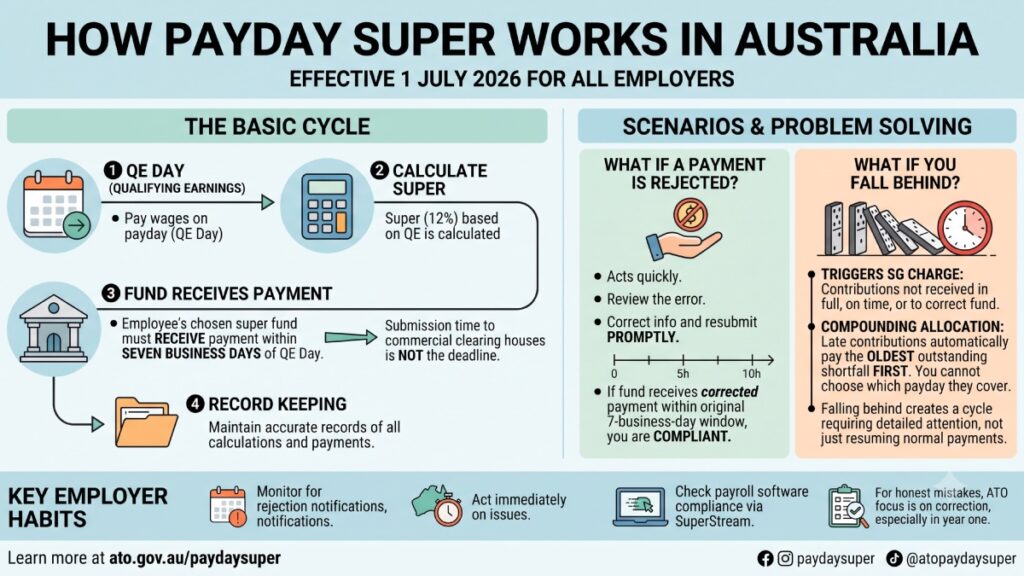

Payday Super is now law. From 1 July 2026, every employer in Australia must pay superannuation contributions within seven business days of each payday, known under the new system as a qualifying earnings day, or QE day. The contribution rate remains 12% of qualifying earnings, which covers payments made to employees for their ordinary hours of work.

For most employers, the ATO is clear that Payday Super does not change the amount of super paid, the employees it is paid for, or the way it is paid through SuperStream. The fundamental change is frequency. Quarterly is gone. Real-time is the new standard.

The practical mechanics are straightforward. An employer pays wages on a given day, that is the QE day. Super calculated at 12% of those qualifying earnings must be received by the employee’s chosen complying super fund within seven business days. Employers using a commercial clearing house need to allow processing time within that window, not treat submission to the clearing house as the endpoint.

The ATO published a worked example to illustrate. An employer pays $3,000 in wages on 10 July 2026. Super of $360 is calculated, paid to the employee’s fund on the same day, and received by the fund on 15 July, well within the seven business day deadline. Records of the calculation and payment are kept. That is a clean, compliant transaction.

Most will go that smoothly. Some will not.

What happens if a payment is rejected

One of the most practical scenarios small business owners will encounter in their first weeks under Payday Super is a rejected contribution. Super funds can reject a payment if the employer has not provided all the required information to allocate the contribution to the employee’s member account.

This does not automatically mean a compliance failure, provided the employer acts quickly. Under the ATO’s guidance, the seven-business-day window runs from the QE day. If a fund rejects a payment and the employer corrects the error and resubmits within that window, the contribution is still on time.

The ATO illustrated this with a specific example. An employer pays wages on 14 August 2026, that is the QE day, giving a deadline of 25 August. The employer submits super on the same day but the fund rejects the payment on 18 August due to missing information. The employer reviews the error, gathers the correct information and resubmits on 19 August. The fund receives it on 21 August, within the seven-business-day window. Compliant.

The lesson for small business owners is to monitor for rejection notifications from super funds actively, particularly in the first months of the new system. A rejection is not automatically a late payment. But ignoring a rejection until it falls outside the window turns it into one.

See Paying super contributions.

What happens if you overpay

Overpayments are handled automatically under Payday Super, and understanding how they work prevents unnecessary concern or confusion.

If an employer pays more than the minimum 12% super guarantee for a given QE day, the excess is automatically allocated by the ATO to the earliest QE day for which the minimum super guarantee has not been paid in full for that employee. If there are no outstanding shortfalls, the excess is carried forward and applied to future QE days for up to twelve months.

The ATO’s example makes this concrete. An employer pays $150 super when the minimum is $120 for a given payday. The extra $30 carries forward. On the next payday, with the same minimum obligation of $120, the employer only needs to pay $90 to meet the super guarantee requirement, though if an award or enterprise agreement requires the full $150, that obligation remains regardless of the super guarantee position.

For employers who pay above the minimum under an award or enterprise agreement, this distinction matters. The automatic allocation satisfies the super guarantee compliance requirement. It does not override the contractual or award obligation to pay the full agreed rate.

If an employee leaves the business and there are excess contributions with no future QE days to apply them to, the employer must contact the employee’s super fund directly to request a refund. Each fund has its own process and will generally require supporting payroll records or contribution details to assess the request.

What happens if you fall behind

Missing the seven-business-day window triggers the super guarantee charge, which applies when contributions are not received by the fund in full, on time and to the right fund. A late contribution, one received after the window but before a super guarantee charge assessment is made, partly reduces the charge but does not eliminate it.

The allocation rule for late payments is automatic and cannot be overridden. Any late contribution is allocated to the earliest QE day for which there is still an outstanding super guarantee shortfall, regardless of what the employer intended the payment to cover.

The ATO illustrated the consequence of this clearly. An employer misses two consecutive fortnightly super payments. When she next makes a contribution on time for her fourth pay cycle, that payment is automatically allocated to the second pay cycle, the earliest outstanding shortfall, leaving the third and fourth cycles still in arrears. The employer cannot direct the payment to the cycle she intended it for.

For small business owners managing tight cash flow, the practical implication is that falling behind on even one pay cycle creates a compounding allocation problem that requires attention to the specific outstanding amounts, not simply resuming normal payments.

What small business owners should do now

The operational guidance the ATO has published reflects the real-world complexity of running payroll across multiple employees, pay cycles and super funds under a new system. The businesses that navigate Payday Super well will be those that treat it as an ongoing operational discipline rather than a one-time setup task.

Checking that payroll software is reporting through SuperStream correctly, monitoring super fund notifications for rejections or allocation issues, keeping clear records of every contribution calculation and payment, and acting immediately when something does not go as expected are the habits that will keep businesses compliant through the adjustment period.

The ATO has been clear that employers who make honest mistakes and take steps to fix them quickly will not be the primary focus of compliance action in the first year. But that goodwill depends on genuine effort to get it right, not on assuming the system will sort itself out.

The official ATO guidance on Payday Super, including payment deadlines, clearing house transitions and super guarantee charge calculations, is available at ato.gov.au/paydaysuper.

Keep up to date with our stories on LinkedIn, Twitter, Facebook and Instagram.