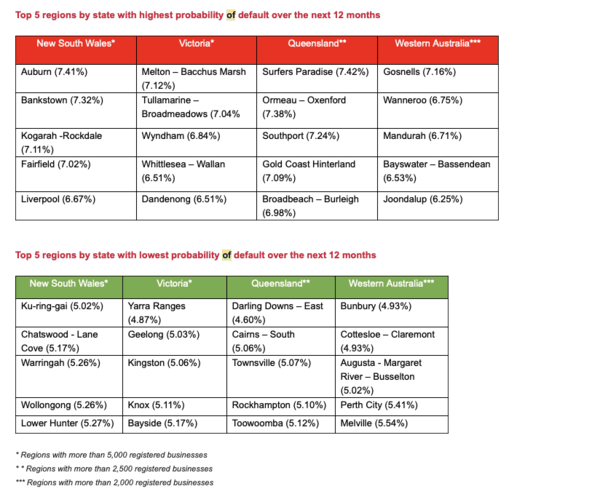

The risk of default over the next 12 months has increased in all regions across Australia owing to labour shortages, rising prices, interest rate hikes, and supply chain problems.

The September 2022 CreditorWatch Business Risk Index (BRI) found that the risk of default over the next 12 months has grown in all regions across Australia with 5000 or more registered businesses, except New South Wales’ Lower Hunter and Wyong regions. Businesses are having a difficult time from the east coast to the west coast.

Highlights:

- Court actions are up 60 per cent year-on-year.

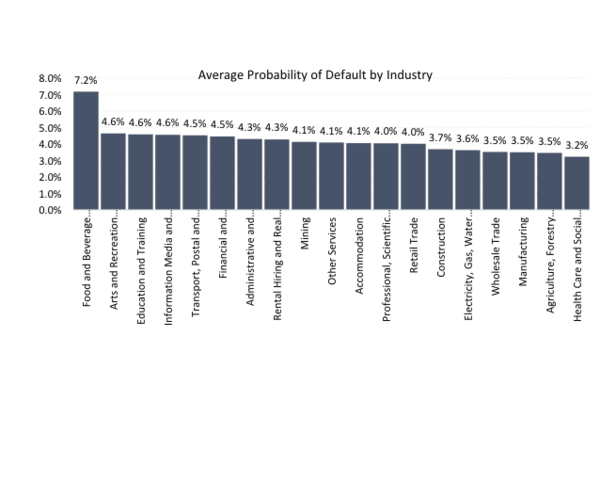

- The industries with the highest probability of default over the next 12 months are: Food and Beverage Services (7.20 per cent); Arts and Recreation Services (4.68 per cent); and Education and Training: (4.63 per cent)

Trade activity still down

A more encouraging development is that year-over-year growth in B2B trade receivables has continued to rise, which suggests that small enterprises’ trade activity has continued to improve since COVID. However, numbers are still much below pre-covid levels.

Trade activity has been steadily falling for some time, but it is now rebounding to more typical levels. The data indicates that there are still restrictions on how our clients are affected by actions that weren’t present before Covid. These restrictions usually come from a lack of goods or a protracted delay in getting them, especially in the construction industry, as well as labour constraints that prohibit expansion or enterprises from working at full capacity.

Therefore, even though both countries’ labour force data are still quite sparse, the data on open positions indicates that firms’ desire to hire new staff has decreased. The RBA is clearly being more careful in its approach to tightening monetary policy as some indications start to show that their cash rate hikes are starting to have an effect. It may take some months before this slowdown starts to show up in labour force data.

CreditorWatch CEO Patrick Coghlan said B2B trade payment defaults showed a dip this month; however, these remain well above levels seen in September last year during Covid and are a lead indicator of future defaults.

“Payment defaults are hugely significant and are a key indicator of coming delinquency for the debtor/customer. Approximately 25% of businesses with default end up in administration within 12 months. Additionally, it puts pressure on the supplier, who will now have to shoulder that bad debt. A business with a trade payment default is seven times the default risk compared to a business with a clean payment record.”

The big picture

There has been a decline in the value of the Australian dollar after the central bank surprised investors by choosing to raise interest rates by a smaller-than-expected quarter point.

The cash rate objective was raised by 25 basis points to 2.60 per cent by the Reserve Bank of Australia. Additionally, it raised the interest rate on Exchange Settlement balances by 25 basis points to 2.50 per cent.

Moreover, the Skills Priority List (SPL) discovered that 286 jobs are now in low supply, up from 153 at the same time in 2021. Nationally, shortages ranged from apiarists, veterinarians, nurses, and teachers to scaffolders, technicians and trades workers, miners, and landscape gardeners. Hotel managers, bus drivers, blacksmiths, and beauty salon managers are among the notable new additions to the skills shortages.

ALSO READ: SME sentiment is weakening despite higher profitability. Here’s why

The announcement verifies many industry groups’ fears about the chronic qualified workforce shortage impeding corporate activity across Australia.

Anneke Thompson, Chief Economist, CreditorWatch says: “Our Business Risk Index (BRI) data for September 2022 was broadly consistent with data trends we have recorded over the preceding months. Trade Receivables continue to increase yearly, indicating that businesses are still feeling relatively confident and that supply and labour bottlenecks are slowly clearing up.

“This month we also saw the Reserve Bank of Australia (RBA) start to move more cautiously through its monetary policy tightening cycle, with only a 25 bps increase in the cash rate. Both monthly Labour Force and quarterly Job Vacancy data that were released recently suggested that the unemployment rate may have reached its trough.

“The unemployment rate increased very slightly to 3.5 per cent, from 3.4 per cent the month prior, while the number of jobs available decreased by 2 per cent (or 10,000 jobs) over the three months to August. This will be welcome news for business owners, most of whom have been struggling to find workers to meet demand. It will also take some pressure off wage increases. Still, job vacancies are at extraordinarily high levels on long-term measures, and it will take many months to normalise.”

As a result of rising fuel and food prices, which have reached a 20-year high, the Australian economy is experiencing difficulties. This year, the RBA has hiked rates six times. Although the RBA left the door open to more hikes as it “assesses the prospects for inflation and economic growth in Australia.”It claimed that it had opted to pause the pace of tightening because the cash rate had been raised significantly in a short period of time.

Way forward

Despite favourable demand and trade circumstances for firms at the moment, analysts are still waiting for consumers to feel the effects of interest rate increases fully.

There are some early indications that, both domestically and worldwide, business conditions have peaked. According to recent ABS Job Vacancy data, there were fewer jobs available in Australia in August than there were in May. Similar trends may be seen in the statistics from the US.

So, while labour force data is still very tight in both countries, the vacancy data suggests that jobs are now starting to be filled at a greater rate, and businesses have slowed their appetite for employees.

It may take some months before this slowdown starts to show up in labour force data, but clearly, the RBA is being more cautious in their approach to monetary policy tightening as some indicators start to show that their cash rate hikes are starting to take effect.

Click here for CreditorWatch Business Risk Index report.

Click here for additional insights into the top and best performers.

Keep up to date with our stories on LinkedIn, Twitter, Facebook and Instagram.